If you have a question about how anything works or have come across something you haven't seen explained here, get in touch with our community of fellow users and Mambuvians where someone will lend a hand.

* If you don't already have an account you will be prompted to create one when you first visit the site.

--- # Card Transactions and Authorization Holds URL: https://docs.mambu.com/docs/card-payments-and-authorization-holds/ Most bank clients today expect to be able to function in a fully cashless way, using debit and credit cards to make and receive payments as well as make direct withdrawals from debit accounts and cash advances against credit. Mambu fully supports industry standard [authorization hold](https://en.wikipedia.org/wiki/Authorization_hold) flows for card payments and allows you to request, adjust, reverse and settle holds against Current Account and Revolving Credit type products. :::note All capabilities for configuring the flow between Mambu and your card acquirer are available [via API only](/api/api-v2/cards/cards). ::: :::warning Card authorization holds are separate from **transaction holds**, which may be applied to any deposit transaction. For more information, see [Transaction Holds](/docs/transaction-holds). ::: ## Requirements * You will need to have the **Cards** functionality enabled for your instance. * A card token reference must be associated with the account. :::note A *card token reference* is used to identify a credit or debit card without needing to always provide sensitive information such as the card number and, as such, is a shared reference between your Mambu tenant and your card issuer’s system.A paragraph.

| 10000 | Assets | |

| 11000 | Fixed Assets | |

| 11001 | Cars | |

| 11002 | Furniture | |

| 12000 | Short Term Assets | |

| 12100 | Cash | |

| 12101 | Cash Branch 1 | |

| 12102 | Cash Branch 2 | |

| 12200 | Bank | |

| 12201 | Bank 1 | |

| 12205 | Bank 2 | |

| Term | Definitions |

|---|---|

Accepted Settlement Completed (ACSC) |

The status of a payment order when it is completed and the SEPA message has been sent to the callout URL. |

Accepted Settlement In Process (ACSP) |

The status of a payment order when it has been executed and the corresponding transaction has been posted in Mambu core. |

Accepted Technical Validation (ACTC) |

The status of a payment order when it has been accepted at the requested execution time. |

account |

A record of all the financial transactions of each of an organization's clients or an organization's assets, liabilities, equity, expenses, and income. In a loan account, Mambu stores all the information related to disbursements, repayments, interest rates, and withdrawals. In a deposit account, Mambu keeps track of all deposits, withdrawals, and the interest rates associated with it. |

account origination |

An upstream component type. Connectors that are part of this component type assist with onboarding new customers, providing access to tools like ID verification, and know your customer and anti-money laundering compliance. |

account servicing institution |

The financial institution that services the account owned by the account holder. In the context of payment orders, both the originator bank and the beneficiary bank are account servicing institutions. |

accrued |

The amount of interest or penalty that has not been paid by the borrower or received by the lender. |

active (account state) |

The status of an account that allows transactions like withdrawals, disbursements, or deposits. A loan account is considered to be active after being disbursed and a deposit account will become active after being approved. Both will remain active until they are closed. |

approved (account state) |

The status of an account after the approval of the account creation request. |

active (client state) |

The status of a client with open accounts in Mambu or a client with no open accounts at the moment but who remains eligible for financial services in an organization. |

administrator (admin) |

A user type in the Mambu UI and API with the most permissions associated with it, by default, users assigned with it can do any operation in Mambu. |

anti-money laundering (AML) |

A general term for policies, laws, and regulations to prevent financial crimes. Global and local regulators around the world create anti-money laundering (AML) policies and requirements. See also know your customer. |

API call node |

A type of node in a Mambu Process Orchestrator process that performs an external API call with parameters. |

API Reference |

The api.mambu.com site, containing all the information required to work with Mambu's APIs. |

arrears |

The status of an active loan account with one or more overdue payments. The Mambu platform lets customers define a specific arrears tolerance period or amount. |

assets |

Items owned by an organization and which have a monetary value associated to them for example, loans, equipment, or cash. |

automated clearing house (ACH) |

An alternate term for a clearing and settlement mechanism (CSM). |

backdate |

To log a transaction that happened on a date earlier than the date on which it took place instead of the current date. |

balance |

The amount of money left in an account after a transaction like a deposit, withdrawal, or repayment. It includes principal, interest, and any available overdraft limit. |

balance sheet |

A financial report that gives a Mambu customer information about their organization's assets, liabilities, and equity at a given point in time. It shows how the organization is performing as well as its value. |

bank |

A general term for a financial institution. Without additional context, "bank" might refer specifically to a traditional bank, or more broadly to nontraditionals and other types of financial institution. |

beneficiary |

The party that receives the funds moved in a payment order that is initiated by the originator. |

beneficiary bank |

The payment service provider (PSP) that processes the payment order received from the originator’s PSP. |

branch |

The default label for an organization's subdivision operating locally or having a particular function. Often branches represent a geographical subdivision of an organization or a product line. Each branch can have multiple centres assigned to it. |

business banking accounts |

Transactional accounts with typical banking capabilities, such as debit or credit cards, for business use. |

business deposits |

Savings accounts, term deposits, and similar products for SMEs or corporations. Examples include savings account, fixed deposit, and savings plan. |

business lending |

Loans made to businesses rather than individuals. See SME lending and commercial lending. |

call process node |

A type of node in a Mambu Process Orchestrator process that calls another process. |

centre |

The default label for a subdivision of a branch. It can be considered a sub-branch. Each branch can have multiple centres assigned to it. |

chart of accounts |

All of the general ledger accounts ordered by their type - assets, liabilities, equities, expenses, or income - and with standard codes associated to each. |

clearing and settlement mechanism (CSM) |

The institution(s) that route funds between accounts as part of a payment order. The clearing and settlement steps might be performed by the involved payment service providers as part of an existing arrangement, or by one or more third parties. |

client |

A single person or entity that is receiving services from a Mambu customer and has a client profile in Mambu. In other words, client refers to the customers of Mambu's customers. |

client ID |

A unique identifier that Mambu automatically assigns to clients when their profile is created. |

closed |

State of an account that doesn't allow transactions anymore. Mambu keeps a closed account associated to the client who owned it. |

code node |

A type of node in a Mambu Process Orchestrator process that executes a block of code. |

collateral |

An asset offered as part of a secured loan to be forfeited in case of default. |

collection order |

An order to transfer money between two bank accounts, initiated by the creditor, based on a pre-existent mandate given by the debtor. Also known as a direct debit transfer. |

commercial lending |

Complex loans for larger corporations often involving high-value principal with multiple credit lines. These loans are used to fund major capital expenditures, operational costs, and/or the purchase of equipment. Commercial loans often require collateral such as property or equipment. |

commercial mortgages |

Collateral-backed loans for commercial real estate. |

composable architecture |

A modular software design methodology consisting of small, self-contained, and easily interchangeable building blocks. An orchestration layer such as Mambu Process Orchestrator directs all interactions between components, providing flexibility and integration with other services. |

composable banking |

Mambu's value proposition using composable architecture to improve the delivery of financial solutions. See also fintech. |

condition node |

A type of node in a Mambu Process Orchestrator process that determines the routing of an object based on a condition. Possible conditions are: equal (=), not equal (!=), less than (<), greater than (>), and regex. |

Configuration as Code (CasC) |

A set of API endpoints that allows customers to batch configure Mambu entities using YAML. Using CasC, customers can quickly configure new Mambu tenants and standardize, version-control, and transfer configurations between tenants. |

connector |

Mambu functionality that allows customers to connect the Mambu cloud banking platform with vetted third-party services via the Mambu Process Orchestrator. Connectors can be built and maintained by Mambu or Mambu partners, and are used to process payments; onboard new customers; manage data and accounting; and more. Connectors might be described as “Integration as a Product.” |

consumer loans |

See purchase financing. |

copy task node |

A type of node in a Mambu Process Orchestrator process that copies a task in a different process. |

counterparty |

The opposite party in a payment order. For example, the beneficiary bank is the counterparty to the originator bank, and vice versa. |

credit (accounting) |

The value entered in accounts which shows a decrease in the assets or expenses or increases in the liabilities, revenue, and capital. |

credit arrangement |

The maximum amount a client (individual client or group) can take out in loans and overdrafts. |

credit cards |

See purchase financing. |

credit officer |

A user type in the Mambu UI and API whose responsibilities are directly related to the management of loan accounts from the application stage till the loan account is closed or withdrawn. Mambu allows users to assign clients to credit officers and keep track of their individual performance. |

credit union |

A cooperative financial institution that is owned and operated by its own members. Credit unions are mostly non-profit and typically provide traditional banking services within a specific community. |

creditor |

The party to which funds are deposited through a credit transaction. |

cryptocurrency |

A digital currency that can be used to buy goods and services, and which uses an online ledger with strong cryptography (typically a blockchain) to record and secure transactions. |

currency |

The form of money used by an organization. |

current account |

An account at a financial institution that supports deposits, withdrawals, and overdrafts. Debit cards can be connected to current accounts. See also daily banking accounts. |

custom field |

A type of additional field that can be created in Mambu UI (that is also accessible via the Mambu API) in order to capture any additional information required for an organization's business processes. Access to custom fields can be restricted to certain roles. Every custom field must be part of a custom field set. Compare with native field. |

custom field set |

A way to group custom fields. |

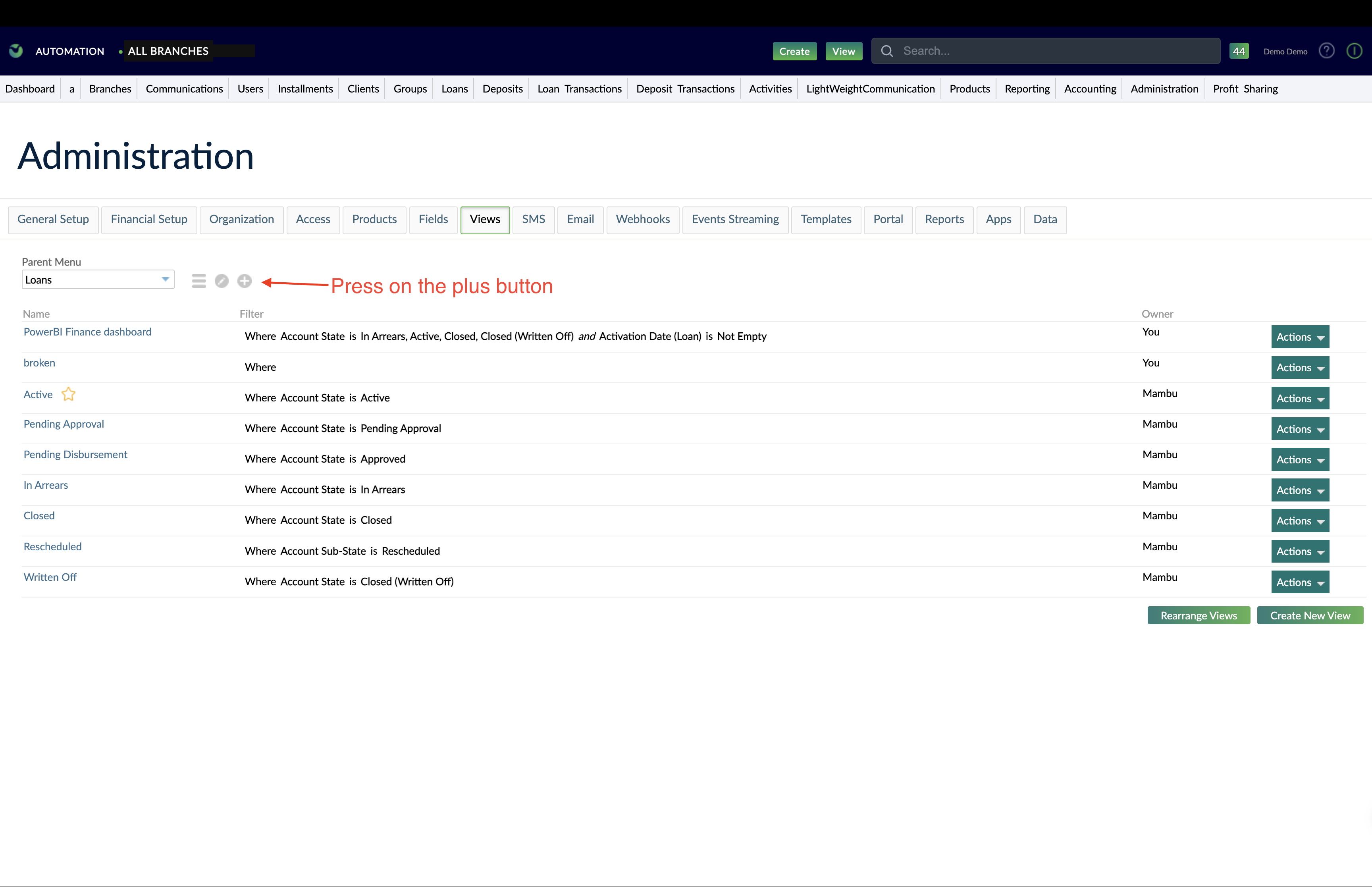

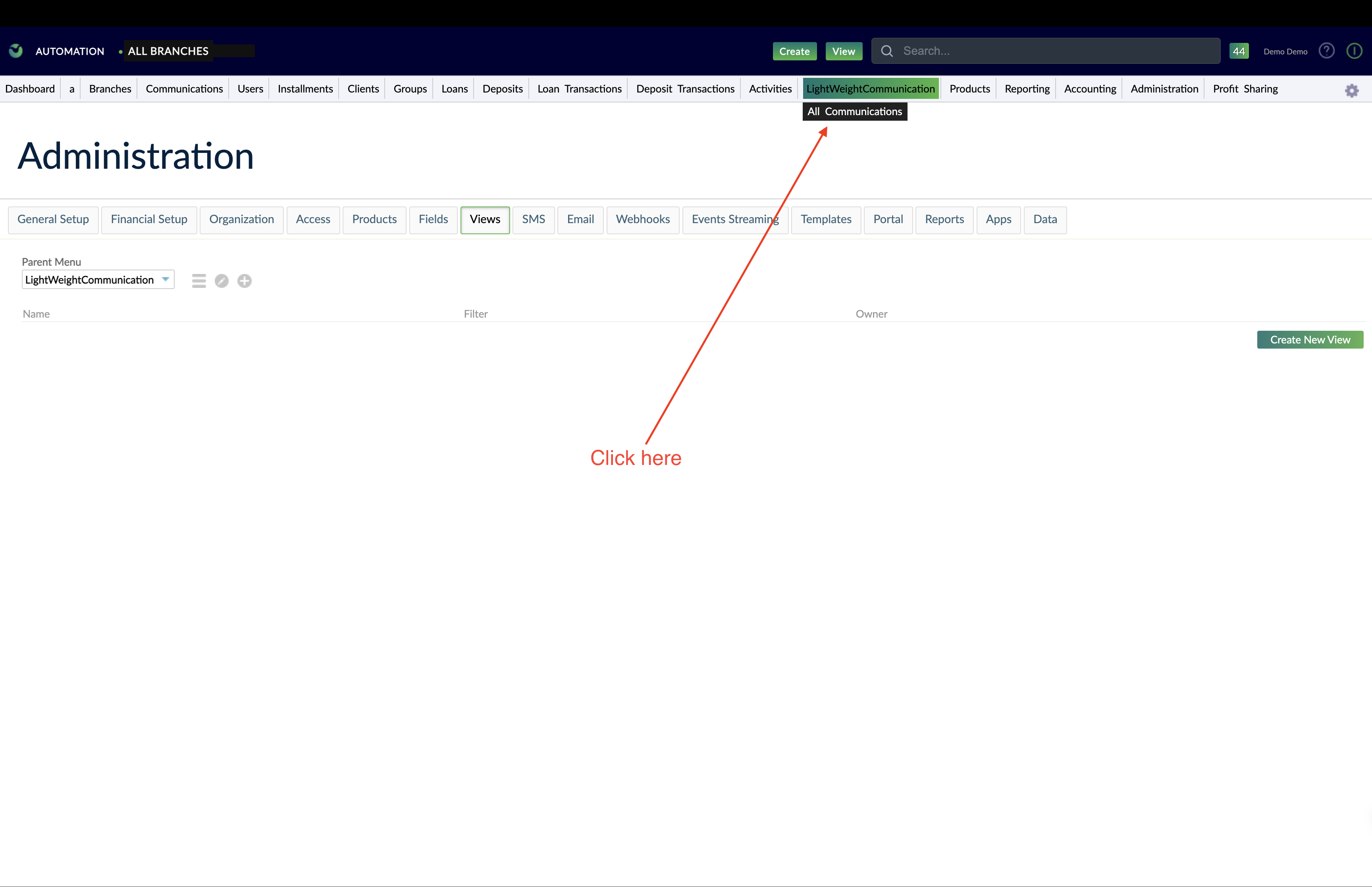

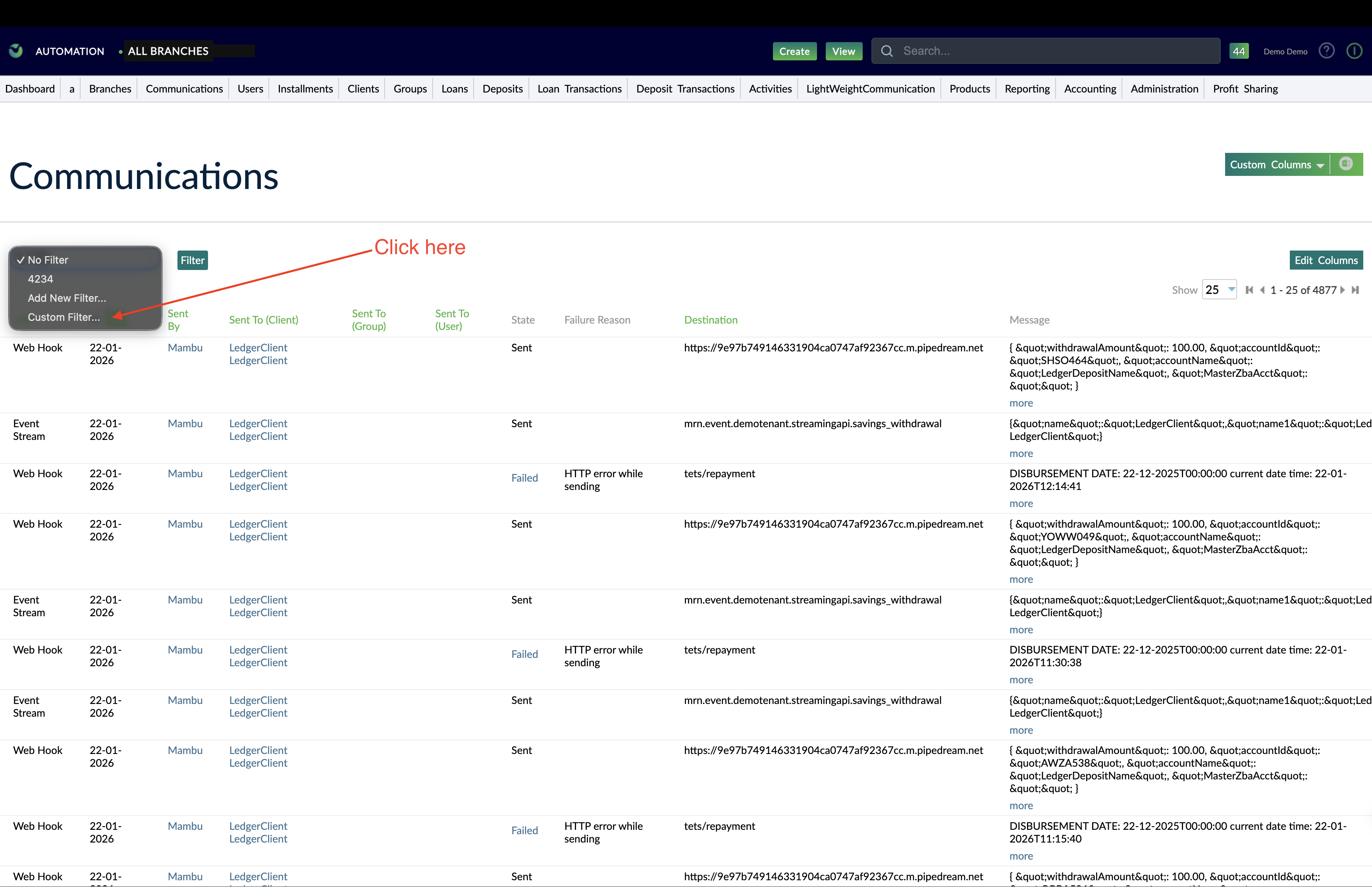

custom view |

A tool to generate reports on the fly and easily retrieve filtered lists of information in the Mambu UI. We refer to custom views as either view or custom view, these terms are interchangeable. |

customer |

An organization that consumes services from Mambu. Customers are associated with one or more instances. |

Customer Service Portal |

The self-service website that allows Mambu customers to manage their support cases, view case reports and dashboards, update contact information, view invoices, perform sandbox operations, and access documentation. |

daily banking accounts |

Transactional accounts with typical banking capabilities, such as debit or credit cards, for personal use. |

debit (accounting) |

The value entered in accounts increasing the assets or expenses or decreasing the liabilities, revenue, or capital. |

debtor |

The party from which funds are withdrawn through a debit transaction. |

dedicated instance |

A Mambu instance that is dedicated to one Mambu customer and is performance-isolated from other customer instances, with all data and services logically and physically isolated. Compare with shared instance. |

delay node |

A type of node in a Mambu Process Orchestrator process that delays a task for a defined period of time. |

deposit |

The amount of money transferred to a client's deposit account. Mambu keeps track of the method used for the transfer such as cash, check, or bank transfer and stores this information in the history of transactions of that specific account. |

deposit account |

An account with an amount deposited by a client to earn interest according to the terms defined in the deposit product. |

deposit product |

A customizable Mambu template used to create individual deposit account instances. Each deposit product represents a collection of settings that differentiates the behavior of deposit accounts. |

detail account |

A category of accounts in the general ledger containing the transaction's balances. |

digital wallet |

A type of stored value account that allows for issuing and managing prepaid instruments. |

disbursement |

The act of releasing the loan amount to the borrower. Mambu identifies the loan account as active and can automatically calculate the loan repayment schedule once disbursed. |

domestic payment |

A payment where the beneficiary is within the same payment network operations region as the originator, using the same currency—for example, a SEPA payment. |

dormant |

The state of a deposit account. In this state no more interest is accrued on the account and no automated transactions can be posted to it. |

downstream data |

A component type for connectors that helps extract and load data into a customer's existing tools (general ledgers, data analytics platforms, etc). |

Early Access |

The stage in the Mambu release cycle, where a feature or capability is available to a limited number of Mambu customers upon their request. |

ecosystem |

See Mambu ecosystem. |

end client |

See client or user. |

end node |

A node used to end a Mambu Process Orchestrator process. There are two types: end: error node and end: success node. |

end user |

See client or user. |

end: error node |

A type of end node in a Mambu Process Orchestrator process that labels tasks with process errors. |

end: success node |

A type of end node in a Mambu Process Orchestrator process that labels successfully processed tasks. |

engine |

A core component of a complex software system, such as the Mambu cloud banking platform itself. |

entity |

A general term for a basic feature, construct, or object in Mambu. Examples include clients, groups, loan products, accounts, currencies, and branches. |

equity |

The organization's value which is property of the shareholders. It corresponds to the value of assets minus the liabilities. |

execution |

See payment execution. |

expense |

The value of assets that is used to sell an organization's services. |

federated authentication |

A form of authentication that allows users to log in to Mambu using single sign-on (SSO). User identities in this scheme are managed by an identity provider (IdP). |

fee |

A fixed price charged to a loan account. |

fiat currency |

An internationally-accepted currency that is usually issued by a government or central bank. It is included in the ISO 4217 currency list. |

field |

A stored value associated with a Mambu entity. For example, a client entity includes fields like ID, Client Type, and Creation Date. Fields can be native fields, which Mambu provides by default, or custom fields, which the user creates. “Field” might also refer to the container in the Mambu UI where a user edits a field. |

financial inclusion |

A broad term to describe the goal of making financial products and services available to all potential clients, regardless of location or income level. Microfinance institutions are a common solutions provider for financial inclusion. |

fintech |

Short for financial technology. A broad term for the industry of technology platforms that compete with traditional platforms to deliver financial products and services. |

fintech (organization type) |

A bank that offers one or more banking products and services without a physical branch network. The term might broadly include neobanks or specifically refer to smaller institutions that focus on selected product lines like remittance or deposits. See also traditional bank and nontraditional. |

fixed deposits |

As the name suggests, fixed deposits have a fixed term after which they should be withdrawn or closed. With this type of product, clients are able to make deposits until the minimum opening balance has been reached. At this point, you can begin the maturity period, during which they will be unable to deposit, but will be able to withdraw. |

foundation platform |

The conceptual component of the Mambu core (alongside the technical platform and product factory) that facilitates services such as output management, notifications, and operational reporting. |

function |

A collection of nodes that Mambu Process Orchestrator can use repeatedly in different processes. |

General Availability |

The stage in the Mambu release cycle where a feature or capability is available to all Mambu customers (provided there is compatibility with the cloud service provider). |

get from queue node |

A type of node in a Mambu Process Orchestrator process that receives tasks from the queue. |

GL code |

The number used to identify an account in the general ledger. |

grace period |

The period of time defined by the number of installments in which the loan repayments don't include interest. The grace period is defined when you're creating loan products. |

group |

A type of client composed of at least two members who also need to have an individual profile in Mambu. |

header accounts |

A category of account that is only used to group detail accounts of the same type. |

identity provider (IdP) |

A service for storing and managing user identities that allows you to connect to Mambu using single sign-on (SSO) when federated authentication is enabled. |

income |

The amount received by an organization for the services provided, sales, or profit from investments. |

Increase Last Installment (ILI) |

A Mambu setting for loan products used to determine what to do with interest in arrears. If Increase Last Installment is selected, Mambu will not adjust the overdue installments, which results in an underpayment of principal. The principal is then recouped in the final installment. |

incumbent |

See traditional bank. |

infrastructure |

The logical arrangement of Mambu's software environment that includes the Mambu core engine and offers networking, database, and other software services. The infrastructure hosts multiple instances that each include multiple tenants. |

installment |

A single scheduled payment for a loan. See also repayment. |

instance |

A logically distinct copy of Mambu's cloud banking platform hosting multiple tenants. Instances are associated with a single Mambu customer, and can be dedicated or shared with other customers. |

interest |

Money paid regularly at a defined rate to a lender or a savings account holder. The interest rate is typically expressed as an annual percentage of the principal, but can also be determined by an external standard. |

interest calculation method |

The formula used to calculate the interest on a loan or savings account. |

internal transfer |

See intrabank payment. |

international payment |

A payment where the beneficiary is from a different payment network operations region from the originator —for example, a SWIFT payment. |

intrabank payment |

A payment where both originator and beneficiary accounts are serviced by the same payment service provider. |

journal entries |

The records of all the transactions in an organization which have accounting implications. They can be automatic or manually entered. |

know your customer (KYC) |

The process of verifying information about clients before or during transactions with a financial institution to confirm their identity, suitability, and risk. KYC rules vary by country and region and are a part of anti-money laundering (AML). |

label |

The terminology used to refer to various entities and concepts within Mambu. Default labels may be edited and labels can be customized for each language available in Mambu. |

lease |

A form of financing in which an institution lends a physical asset or service to an individual or business client for defined payments and duration, sometimes with a provision to purchase the asset at the end of the contract. Leases can be issued by single-purpose leasing companies or by larger banks. |

leasing company |

A company that offers leases on physical assets or services. Unlike traditional banks or other financial institutions, leasing companies are single-purpose companies. |

lender |

The financial institution that offers loans to borrowers. Lenders might be single-purpose institutions or larger institutions that offer additional financial products, for example, traditional banks. |

lending |

The temporary giving of money or assets to a borrower (a loan) with an agreement that it will be repaid according to certain terms and conditions. Mambu offers a variety of lending products. |

liabilities |

What an organization owes to others both currently and in the future. For example, clients deposits are considered to be a liability as the amount will be returned to the clients. |

loan |

The amount that an institution lends to a client; or the loan account that corresponds to the loan and specifies the loan terms and conditions. |

loan account |

In Mambu, an individual account used to track the corresponding loan and client. Terms and conditions that you define when creating a loan product—interest rates, the repayment schedule, applicable fees, and so on—apply to all of the loan accounts created using that product. |

loan origination (connector type) |

A Mambu connector component type that provides tools for managing applications, credit decisioning, and responding when loans go into arrears. |

loan product (Mambu template) |

A customizable Mambu template used to define and create individual loan accounts. |

loan rescheduling |

An operation used in Mambu to refinance a loan (by changing the interest rate and capital amount), restructure it (by changing the payment frequency or term), or both. |

Mambu Apps |

An integration to create selectable frames in the Mambu UI that render an externally-hosted application’s data. |

Mambu Champion |

An employee at the organization that receives services from Mambu (one of Mambu's customers) who is designated as the primary contact for Mambu and its partners. |

Mambu cloud banking platform |

The collective functionalities of Mambu’s core banking software including the Mambu core, Mambu Process Orchestrator, connectors, and so on. |

Mambu core |

The central piece of the Mambu cloud banking platform representing Mambu software itself. The Mambu core consists of the foundation platform, technical platform, and product factory (including the deposit engine and lending engine). The Mambu core interacts with the rest of the Mambu ecosystem using Mambu Process Orchestrator. |

Mambu display language |

The language a user chooses to see displayed in Mambu. |

Mambu ecosystem |

The composable and modular framework that integrates the Mambu cloud banking platform and Mambu Process Orchestrator with third-party financial service providers. |

Mambu Payment Gateway (MPG) |

The component that facilitates one-time and recurring transactions using the Single Euro Payments Area (SEPA) scheme. It has its own interface for configuration, managing users, and auditing transactions, and its own suite of APIs for making, receiving, rejecting, and refunding standards-based payments. |

Mambu Process Orchestrator (MPO) |

The orchestration layer that enables Mambu customers to exchange data between the Mambu core and other API-enabled systems. |

Mambu UI |

The graphical user interface for Mambu itself. |

Mambu User Guide |

The support.mambu.com site, with comprehensive documentation about Mambu’s products, with a particular focus on the Mambu UI. |

MambuCast |

A webinar series produced by Mambu Partner Enablement to train Mambu partners on a variety of topics. |

maturity |

The date on which a fixed deposit becomes due, meaning that it won't continue to accrue interest and the clients can withdraw their money with the already accrued interest. |

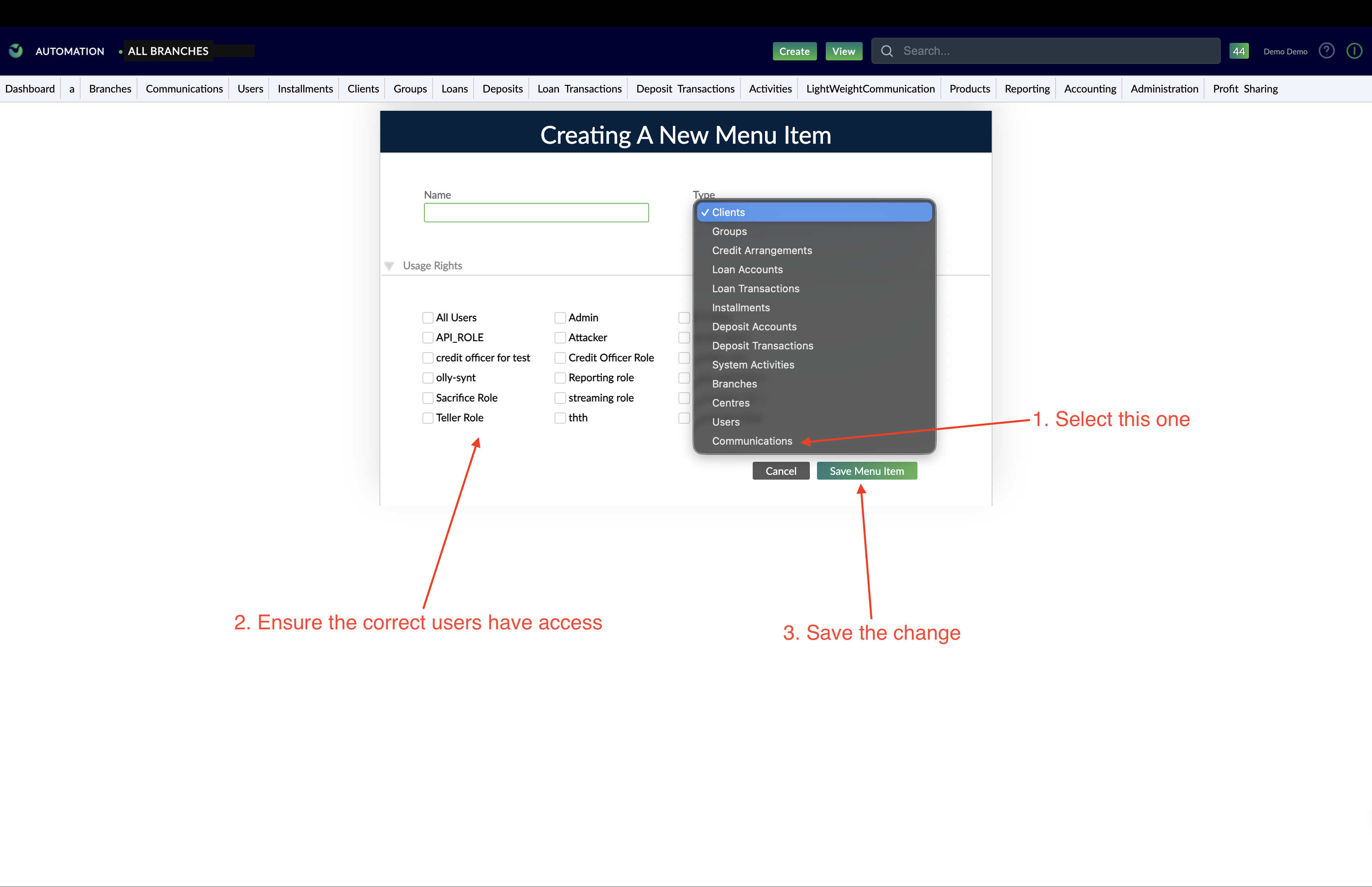

menu item |

An option on the navigation bar in the Mambu UI. There are two categories of menu items: menu items with views and menu items without views. Views are also referred to as custom views, these terms are interchangeable. |

microfinance institution (MFI) |

A financial institution that serves individual or business clients who lack access to conventional financial services, typically low-income or geographically isolated clients. See also financial inclusion. |

modify task node |

A type of node in a Mambu Process Orchestrator process that updates a task in another process. |

mortgage |

A secured loan used either to buy real estate or to raise funds against the value of owned real estate. For the relevant Mambu product, see retail mortgage. |

mortgage with redraw facility |

A mortgage that allows the borrower to make payments higher than the minimum schedule requires. These additional payments can either be withdrawn at by the borrower at a later date or be applied to the interest due over the term of the loan. |

multi-tenancy |

The ability for a single Mambu software instance to support multiple tenants. |

native field |

A field in the Mambu UI (that is also accessible via the Mambu API) that is both part of an entity by default and is accessible to any user of that entity. Compare with custom field. |

neobank |

A bank that offers traditional banking products and services without a physical branch network. Neobanks might have a formal relationship with traditional banks or operate independently and compete with them. See also nontraditional and fintech (organization type). |

node |

A logical unit that executes an action. Nodes are used to create a process in the Mambu Process Orchestrator. |

Non-Production Preview |

The stage in the Mambu release cycle where a feature or capability is available to a limited number of Mambu customers chosen by Mambu. |

non-traditional currency |

An alternative store of value that a user can define in Mambu. Examples of non-traditional currencies include loyalty points, such as Amazon Coins, and pseudo-currencies, such as the Unidades de Inversion (UDIs) used in Mexico to protect investments from high inflation. |

nontraditional |

A smaller, newer financial institution that might offer lending or deposit services, but not both. Examples include e-commerces, telcos, and retail outlets that offer financial services like credit cards, buy-now-pay-later options, consumer lending, and so on. See also neobank and traditional bank. |

offset mortgage |

A mortgage that is linked to a savings account held by the same financial institution. The savings account balance is used to reduce, or “offset,” the mortgage interest that the borrower is charged. |

orchestration layer |

The software in a composable architecture system that exchanges data between architecture components. Mambu Process Orchestrator (MPO) is the orchestration layer between the Mambu core and third-party services. See also downstream systems and upstream systems. |

organization |

A Mambu customer, including staff members and the different branches. |

originator |

The party that initiates a payment order that is received by the beneficiary. |

originator bank |

The payment service provider (PSP) that services the originator's account. They receive the payment order instruction from the originator, in order to be executed and sent towards the beneficiary’s PSP. |

outstanding principal |

The amount of principal on a loan that remains to be repaid. |

overdraft |

A deficit in a bank account caused by withdrawing more money than the account holds. The institution that manages the account may charge fees or higher interest rates when an account is overdrafted. |

partner accreditation |

Mambu's program to train partners on working with Mambu and its customers. Accreditation is appropriate for sales and solutions partners, and also for services partners when partner certification is not yet available. |

partner certification |

Mambu's program to train partners to serve existing Mambu customers. Certification training includes lab components and a proctored exam and is intended for services partners who work directly with customers. |

Partner Enablement |

Mambu's organization for training current and future Mambu partners. Enablement products include partner accreditation and partner certification. |

payment execution |

The process of moving money from the originator account to the beneficiary account as specified in a payment order. When executing a payment, Mambu determines whether both accounts are in Mambu and selects the appropriate processing mechanism. |

payment network operations region |

A single country, multiple countries, or an economic bloc where payments are settled in the same manner, through the same mechanism. |

payment order |

An order to transfer money between two bank accounts: the originator account and the beneficiary account. Also known as a credit transfer. |

payment order initiation |

The process of submitting a payment order for subsequent execution. |

payment processing |

A connector component type that helps the Mambu cloud banking platform integrate with payment processing and transaction monitoring services. |

payment service provider (PSP) |

The financial institution that services an account sending or receiving a payment order. Terms like "bank" or "financial institution" might be used to describe a payment service provider. |

Mambu Payments Gateway API |

An API available through Mambu’s API Reference that allows customers to process domestic and international payments made via the Single Europe Payments Area (SEPA) payments scheme. |

peer-to-peer (P2P) lending |

A lending platform that connects lenders with borrowers. Either party in peer-to-peer lending (P2P lending) might be a business or individual. The P2P lending platform does not lend money, but establishes loan terms and conditions. |

penalty |

A defined fee that an organization may charge to clients when a specific term of the loan contract is violated—most commonly, when the client is late repaying a loan. |

permission |

The authorization given to users that enables them to view a type of information or to perform an action in the Mambu UI or via the Mambu API. Permissions can either be assigned directly to users or assigned to them through a role. |

personal deposits |

Savings accounts and term deposits for individuals. |

personal lending |

Interest-bearing personal loans for individual use. Personal loans can be secured or (in most cases) unsecured, meaning they are not backed by collateral. Examples include microfinancing, payday loans, cash advances, and car and boat loans. |

prepaid card account |

A type of stored value account that allows issuers to store monetary value onto prepaid cards. A prepaid card is not linked to a bank account. |

Prepayment Recalculation Methods |

A Mambu setting to adjust how to handle prepayment of a loan, regarding recalculating the loan principal and repayment schedule. |

principal |

The original amount borrowed for a loan or deposited in an interest-bearing account, excluding interest, fees, and penalties. See also outstanding principal. |

process |

A series of actions built in Mambu Process Orchestrator from individual nodes. |

product |

Any specific type of loan or deposit that an organization creates for its clients. Any loan account or deposit account will be part of a product, so the terms and conditions defined when a product is created will then be used to set the constraints of the account. |

product actions |

Actions that represent the transactions that are automatically logged by Mambu, once products are linked to general ledger accounts. |

product factory |

The product configuration engines—lending engine and deposit engine—that Mambu customers use to create a new product using pre-defined parameters. The product factory is one of the three components of the Mambu core alongside the technical platform and foundation platform. |

production |

A tenant provided by Mambu which is used for processing end-client data. It's the live application. Also known as production tenant. |

purchase financing |

Consumer finance loans offered by a business or retail e-commerce to its clients, such as point-of-sale financing, “buy now pay later” programs, or credit cards. |

queue node |

A type of node in a Mambu Process Orchestrator process that implements queue logic. |

Received (RCVD) |

The status of a payment order when it has been received and the input has been validated. |

reduce amount per installment (RAI) |

A method to recalculate the schedule by reducing the installment amount when a client makes a prepayment. |

reduce number of installments (RNI) |

A method to recalculate the schedule by reducing the number of installments when a client makes a prepayment. |

Rejected (RJCT) |

The status of a payment order when it has been rejected. |

repayment |

The amount that borrowers need to pay on a loan as determined by a repayment schedule. Repayments can include principal, interest, fees, and penalties. |

Repayment Schedule Versioning (RSV) |

A system for tracking the history of repayments on a loan in Mambu. |

reply to process node |

A type of node in a Mambu Process Orchestrator process that replies to a call from another process. |

retail mortgage |

A collateral-based mortgage for individuals. Despite the name, retail mortgages are for non-commercial real estate. |

RFI |

Short for Request for Information. A request to suppliers for information on the products and services that they can provide, typically used to gather information about potential future suppliers. RFIs are typically followed by an RFP or RFQ. |

RFP |

Short for Request for Proposal. A request that describes a project and solicits bids to complete it. An RFP is appropriate when the requester doesn't know specifically how they want to solve a problem. |

RFQ |

Short for Request for Quotation. A request for pricing proposal for a particular product or service, appropriate when the requester has a specific solution in mind but not how much it will cost. |

RFX |

Short for Request for X. A blanket term for RFP, RFI, and/or RFQ. |

role |

A way to group permissions and to control other forms of access within Mambu UI and API. Each user in Mambu may be assigned a role. The user will then have all the permissions that are a part of that role. Also known as user role. |

sandbox |

A tenant within a given Mambu instance that customers can use for development and testing. Also known as sandbox tenant. |

savings accounts |

Individual tenants associated with a Mambu deposit product. Savings account holders typically earn interest and can make deposits and withdrawals when they wish. For the relevant Mambu products, see personal deposits and business deposits. |

savings plan |

A savings product that allows a client to make deposits during the maturity period, but not withdrawals. Once the maturity period ends, a client can make withdrawals but not deposits. |

schedule |

The repayment plan for a loan, typically including repayment amounts, dates, accrued interest, and required fees. |

secured loan |

A loan whose value is secured by collateral. |

SEPA |

Short for Single Euro Payments Area. An EU initiative to integrate euro-based transfers between banks in EU and other participating countries. |

set parameter node |

A type of node in a Mambu Process Orchestrator process that sets or modifies a parameter value in the task. |

set state node |

A type of node in a Mambu Process Orchestrator process that implements storage logic and task state distribution. |

shared instance |

A Mambu instance shared among multiple Mambu customers, each with its own isolated data and configuration. The workload of all tenants in the instance is spread across the same infrastructure and software processes. Compare with dedicated instance. |

single sign-on (SSO) |

an authentication scheme, available when federated authentication is enabled, that allows users to log into multiple systems with a single identity. |

SME lending |

Interest-bearing secured or unsecured loans granted to small and medium-sized enterprises (SMEs) to help them to start or expand their business or support their operational needs. Examples include working capital loans, term loans, and SME lines of credit. |

sponsor bank |

A bank that is a member of an approved bank card system such as Visa or Mastercard. Sponsor banks offer credit cards and other lending options related to the bank card system. |

state (loan and deposit account) |

The stage of an account in an organization. Loan accounts can be in a pending approval, approved, active, active (in arrears), closed (with obligations met), closed (rescheduled) or closed (written off) state. Deposit accounts can be in a pending approval, active, closed, or dormant state. |

stored value accounts |

Transactional accounts that support digital wallets or prepaid card accounts. Stored value accounts don't offer typical bank account features like interest. |

Streaming API |

An API available through Mambu’s API Reference that allows customers to subscribe to real time data streaming from Mambu. |

sum node |

A type of node in a Mambu Process Orchestrator process that adds up a series of values and returns the sum. |

task |

A logical set of parameters that represents data passing through the nodes of a process in the Mambu Process Orchestrator (MPO). The MPO routes and transforms the task according to the logic and functions of the nodes. |

technical champion |

An employee at the organization that receives services from Mambu (a customer) who is designated as the primary contact for the integration consultant and other technical contacts at Mambu. |

technical overdraft |

See overdraft. |

technical platform |

The conceptual component of the Mambu core (alongside the foundation platform and product factory) that includes supporting services such as account sub-ledgers, customer information, and access management. |

teller |

A user type in the Mambu UI and API that represents the “front office” customer service in financial institutions that are usually responsible for processing client transactions, such as making deposits or withdrawals or processing loan repayments and disbursements. |

tenant |

A logically isolated access point in a Mambu instance with its own URL, database, accounting, and configuration. Each instance includes at least two tenants (production and sandbox) but supports more if needed (for example, a bank operating in multiple regions). |

total due |

The loan amount due to be paid by the borrower, factoring in the loan principal, interest, fees, payments, and penalties. |

traditional bank |

A typical financial institution that handles both individual and business clients. Most traditional banks maintain a physical presence and often employ older technology. See also neobank and nontraditional. |

transaction |

Any operation implying changes in the balance of an account such as deposits, withdrawals, or disbursements. Mambu tracks all transactions and associates them to the clients' accounts where they occurred. |

unauthorized overdraft |

See overdraft. |

unsecured loan |

A loan that is not secured with collateral. |

user |

Anyone who accesses and uses Mambu via the UI or the API. Each user has a user account with unique credentials and may have a role, user type, and/or permissions assigned to them. |

user type |

A user setting in the Mambu UI and API that assigns certain access settings to a user or an API consumer. There are three available user types, administrator, credit officer, and teller. |

username |

A short identifier, usually an abbreviation of the user's name which is determined when the their profile is being created in the Mambu UI or API. |

waiting for callback node |

A type of node in a Mambu Process Orchestrator process that requests and waits for a response from an external system. |

withdrawal (deposit account) |

The action of taking money out of a deposit account. |

withdrawal (state) |

The removal of a loan application from Mambu. |

write-off |

The action of closing a loan account after determining that the amount won't be recoverable. Written off loans will be automatically considered as an expense for accounting purposes. |

BRANCH_VIEW: Shown as a tab under a branchCENTRE_VIEW: Shown as a tab under a centreCLIENT_VIEW: Shown as a tab under clients' profilesDEPOSIT_ACCOUNT_VIEW: Shown as a sub-tab for clients' deposit accountsDEPOSIT_PRODUCT_VIEW: Shown as a tab under a deposit productEXTENSION_MENU: Shown as a drop-down menu item under the App viewGROUP_VIEW: Shown as a tab under a group's profileLINE_OF_CREDIT_VIEW: Shown as a sub-tab for clients' credit arrangementsLOAN_ACCOUNT_VIEW: Shown as a sub-tab for clients' loan accountsLOAN_PRODUCT_VIEW: Shown as a tab under a loan productREPORTING_VIEW: Shown as a tab under the reporting view USER_VIEW: Shown as a tab under users' profiles/ > < | : & ? * [ ] # \* `**

:::

## Managing documents

You can make changes to the title and description of the documents, download them to your local machine, or simply delete them.

### Previewing documents

To preview a document:

1. Open the loan account.

2. Go to the **Attachments** tab.

3. In the list of documents, find the one you want to preview and, on the right-hand side of the row, select **Actions** > **Preview**.

### Downloading documents

To download a document:

1. Open the loan account.

2. Go to the **Attachments** tab.

3. In the list of documents, find the one you want to download and on the right-hand side of the row, select **Actions** > **Download**.

Or, you can click directly on the document name.

### Editing documents

To edit a document:

1. Open the loan account.

2. Go to the **Attachments** tab.

3. In the list of documents, find the one you want to edit and on the right-hand side of the row, select **Actions** > **Edit**.

4. Make the desired changes.

5. Select **Save Changes**.

### Deleting documents

To delete a document:

1. Open the loan account.

2. Go to the **Attachments** tab.

3. In the list of documents, find the one you want to delete and on the right-hand side of the row, select **Actions** > **Delete**.

4. Confirm.

---

# Loan account goes in arrears

URL: https://docs.mambu.com/docs/loan-account-goes-in-arrears/

## Business case

A 3rd party system must be notified when a loan account with a loan amount higher than 1 million goes into arrears. This will apply for individual clients only. The receiving end is exposing an API which is able to receive POST calls with a JSON payload containing the client id, loan id, the current date when the loan goes into arrears, and the loan amount.

***

## Configuration

***

---

# Loan Account Life Cycle and States

URL: https://docs.mambu.com/docs/loan-account-life-cycle-and-states/

From the moment you create a new loan account, it will go through different states, each of them with specific implications which are shown in the following diagram and described in more detail below.

:::warning

For all the examples below, the underlying assumption is that users have the right permissions to perform each of the actions.

:::

## Set up the initial state of a loan account

When [setting up a new loan product](/docs/setting-up-new-loan-products), in the **New Account Settings** section of the form, choose what you want the initial state of the account to be: `Partial Application` or `Pending Approval`.

### Partial Application

When a loan is in `Partial Application`, it means that the loan application is missing information and is not yet complete.

As soon as all the documents are collected and the application is complete, you can request approval which will set the loan account to `Pending Approval` state, so that it can be evaluated.

If at this stage a decision is made not to proceed with the application at all, it can be `Rejected` by the organization or `Withdrawn` by the client.

:::note

In this state it is still possible to edit the loan account terms, such as loan amount, interest rate, or number of installments.

:::

### Pending Approval

When a loan is `Pending Approval`, it means that the loan application is under evaluation and can be either:

* Approved

* Rejected (by the organization)

* Withdrawn (by the client)

* Set as Incomplete (if there is still information or documentation missing from the application, you can send the application back to `Partial Application`).

:::note

In this state it is still possible to edit the loan account terms, such as loan amount, interest rate, or number of installments.

:::

### Reject an application

When an application is `Rejected`, the account will be automatically closed and classified as `Closed (Rejected)`.

The loan account will remain associated to the client or group who requested it and all the information that was entered, like comments or notes will remain associated to the account allowing you to keep track of the reasons for the rejection.

This information can be used later, in case the client makes a new request and you want to consider it for the new evaluation process.

:::note

You can **Undo Reject** and send the account back to its previous state by selecting the option available under **More**.

:::

### Withdraw an application

If the client chooses to **Withdraw** the loan application, it will be automatically closed and classified as `Closed (Withdrawn)`.

:::note

You can **Undo Withdraw** and send the account back to its previous state by selecting the option available under **More**.

:::

## Approved

Once all the account terms are evaluated and agreed upon, the loan application can be approved.

To approve a loan account, select **Approve**, add any comments you might have and confirm.

After being approved, the loan terms such as loan amount, interest rate, or number of installments cannot be changed anymore.

At this stage, the loan can either be `Disbursed` or can be `Withdrawn` by the client.

:::note

You can **Undo Approve** and send the account back to its previous state by selecting the option available under **More**.

:::

### Disburse a Loan

As soon as the application is approved, it's ready to be disbursed.

After being disbursed the loan account becomes automatically `Active`.

:::note

You can **Undo Disbursement** and send the application back to the `Approved` state by selecting the option available under **More**.

:::

## Active

This is the state of an account immediately after being disbursed.

It will remain in the `Active` state as long as the account remains in good standing.

## Active (in Arrears)

When a loan account has at least one late repayment, Mambu will automatically change its state to `Active in Arrears` until all repayments are made.

The late repayments will then be displayed under each account's repayment schedule.

## Locked

When there are unexpected events, or a client is having problems repaying a loan, you can lock the account and suspend interest, penalties and fees from being applied on the account.

When the account will be unlocked, the interest, fees and penalties that were accrued during the account locked state will be applied on the account.

## Terminated

When you terminate a loan, the total outstanding principal plus all accrued charges become due immediately (as of the termination date).

This feature is currently available for:

* Dynamic Loans

* Interest calculation method: Declining Balance Equal Installments

* Pre-payment allocation: On upcoming pending installment only

* Pre-payment recalculation: Reduce Number of Installments (RNI)

* Pre-payment recalculation: Reduce Amount per Installment (RAI)

* Types of fee allowed: Manual Fees only

To terminate a loan account, select **Close** > **Terminate**.

Add any notes you wish to this transaction for auditing purposes. These notes will be stored with the history of transactions for this account.

:::note

You can **Undo Terminate** and send the loan account back to its previous state by selecting the option available under **More**. The interest will still be applied, though.

:::

## Closed

Loan accounts can be closed in several situations presented below.

### All Repayments Made

When the client finishes repaying all the installments, the account can be closed and will be stored under the client's profile as `Closed (all obligations met)`.

:::note

Mambu will automatically calculate the "Completed Loan Cycles" whenever a loan account is closed with "All Obligations Met", meaning the loan has been either fully repaid or paid-off early.

:::

### Paid Off

When a client pays the whole amount of the loan earlier, the account can be closed for that client.

To pay off a loan account, select **Close** > **Pay-off**.

If part of the outstanding loan amount is not collected, you can choose to write off any remaining balances for interest, fees and penalties.

Add any notes you wish to this transaction for auditing purposes. These notes will be stored with the history of the transactions for this account.

The paid-off loan account will be stored under the client's profile as `Closed (all obligations met)`.

### Writen Off

When repayments are no longer expected on a loan account that is in arrears, it should be closed and written off.

To write off a loan account, select **Close** > **Write off**.

Add any notes you wish to this transaction for auditing purposes. These notes will be stored with the history of the transactions for this account.

The written-off loan account will be stored under the client's profile as `Closed (Written Off)`.

### Rescheduled

If for instance, due to an unexpected event, a client is having problems repaying a loan, you can choose to reschedule the loan, therefore adjusting its terms in order to prevent it from going into arrears.

To reschedule a loan, select **Close** > **Reschedule**, add notes about the reasons for rescheduling and confirm the new state.

When you reschedule a loan, the current loan will be closed, its state will change to `Closed (Rescheduled)` and a new loan with the new terms will be automatically created with a link to the original account (this is often a requirement in an auditing process).

If the rescheduled account had interest, fees or penalties due, you can choose to either capitalize them on the new account principal balance or to writte them off when the new loan account is created.

### Refinanced

If you decide to top-up a loan account, you can choose to refinance the loan by adding an additional amount to the current balance of the loan.

To refinance a loan, select **Close** > **Refinance**, add notes about the reasons for refinancing and confirm the new state.

When you refinance a loan, the current loan will be closed, its state will change to `Closed (Refinanced)` and a new loan account with the new terms will be automatically created with a link to the original account (this is often a requirement in an auditing process).

If the refinanced account had interest, fees or penalties due, you can choose to capitalize them on the new account principal balance or to write them off when the new loan account is created.

---

# Loan Account Overview Details

URL: https://docs.mambu.com/docs/loan-account-overview-details/

Balance information can be retrieved from a loan account via API v2 by using the [Loan Accounts - getById](/api/api-v2/loans/get-by-id) endpoint. The same information is also available in the UI account overview, under **Details**.

| Balance | Description |

| --- | --- |

| **Total Balance** | The total amount of the loan, which consists of the principal plus any interest, fees, and penalties that may have been charged. |

| **Principal Balance** | The total amount of principal. |

| **Interest Balance** | The total amount of interest. |

| **Interest from Arrears Balance** | The total amount of interest from arrears. |

| **Interest Accrued** | The amount of interest accrued by the current date. |

| **Interest from Arrears Accrued** | The amount of interest accrued from arrears by the current date. |

| **Fee Balance** | The total amount of fees. |

| **Total Due** | The total amount that is currently due. |

| **Principal Due** | The principal amount that is currently due. |

| **Interest Due** | The interest amount that is currently due. |

| **Interest from Arrears Due** | The interest from arrears amount that is currently due. |

| **Fees Due** | The total amount of fees that is currently due. |

| **Penalty Due** | The total amount of penalties that is currently due. |

| **Total Paid** | The total amount that has been paid. |

| **Principal Paid** | The total principal amount that has been paid. |

| **Interest Paid** | The total interest amount that has been paid. |

| **Interest from Arrears Paid** | The total interest from arrears that has been paid. |

| **Fees Paid** | The total amount of fees that has been paid. |

| **Penalty Paid** | The total amount of penalties that has been paid. |

## Days in arrears vs. days late

There is a difference between how many days an account is in arrears and how many days an account is late. In the example provided in the screenshot, a grace period of 12 days was set up.

* **Days in Arrears**: For products with no grace period, a loan account will be marked as `In Arrears` from the day following the due date. For products with grace period, the days in arrears will be counted from the day following the arrears tolerance period.

* **Days Late**: If a loan has a grace period, the loan will intially be marked simply as late. The days late are calculated from the day following the due date.

## Regular interest vs. late interest

In the **Details** section of the loan account, you can also see more information about interest from arrears including how much of the total interest comes from interest from arrears. Here is the difference between the regular interest and the late interest:

* **Interest Balance**: shows the total interest.

* **Interest from Arrears Balance**: shows how much of **Interest Due** is coming from arrears.

* **Interest from Arrears Accrued**: shows how much of **Interest Accrued** is coming from Arrears.

:::note

* **Interest Balance** already contains **Interest from Arrears Balance**.

* **Interest Accrued** already contains **Interest from Arrears Accrued**.

:::

## Foreign currency loans

When your tenant is first created, you will be asked to choose a base currency. Later on, you may create additional fiat, crypto, and non-traditional currencies which you will use to create your products and accounts. For more information, see [Currencies](/docs/currencies). Foreign currency loans are loans in a currency other than you base currency. Foreign currency loans is an early access feature.

:::note

You can make transactions between loan accounts and deposit accounts only if their respective GL accounts are set in the same currency.

:::

---

# Loan Auto Approve workflow

URL: https://docs.mambu.com/docs/loan-auto-approve-workflow/

## Business case

Approve a loan account of an individual client if the client has at least 5 years of service at at the current working place, the loan amount is greater than 1000 and the credit score captured at account level is greater than 2.

:::warning

In the conditions outline below, there is an `Account State` check which is not part of the business criteria but instead is necessary from a technical point of view. This check serves to prevent API calls from being made for every account activity performed after the account is approved, since the other conditions would then already have been met. This is referred to as a "notification breaker" criteria.

:::

***

## Configuration

***

---

# Loan Fees Setup

URL: https://docs.mambu.com/docs/loan-fees-setup/

Fees can be applied to loan accounts after being created or activated under each product.

## Setting up a new fee

To set up a new loan fee:

1. When creating a new loan product or editing an existing loan product, go to the **Product Fees** section of the form.

2. Select **Add Fee**.

3. Enter the name of the fee (this is the name that will be shown in different screens, when applying the fee to the account, when reporting, in the account statements, and so on).

4. Select the type of the fee (see more details about each fee type below).

5. Enter an Id for the fee. If you leave this field empty, an id will be automatically generated.

6. Define how the amount of the fee will be calculated, either as a fixed amount or as a percentage (the available calculation options will differ depending on the fee type).

7. Select if the fee is **Optional** or **Required** (only available for certain fees).

8. If accounting is enabled, and if applicable, select the specific General Ledger (GL) accounts.

After fees are applied to an account, they will be paid according to the [allocation order](/docs/repayment-allocation-order) defined for that product.

## Deactivating and reactivating fees

If a fee is not applicable anymore, you can deactivate it by selecting the small green square next to it and then saving your changes. When the fee is deactivated, the small green square will turn from green to grey.

To reactivate a fee, follow the same procedure: select the grey square, then save your changes. When the fee is reactivated, the small grey square will turn from grey to green.

## Deleting fees

Fees can be deleted only if they have never been applied to any account. This option is only available for specific cases when a fee was created by mistake and we strongly recommend you to use it with care.

To delete a fee, select the red **Delete** button next to the fee name, then save your changes.

If the fee has already been used and you try to delete it, Mambu will show you a warning message preventing you from doing so. In that case, you must **Deactivate** the fee. After you deactivate the fee, it will no longer be applied to any accounts created under that product.

## Nontaxable fees

Nontaxable fees are available for *Dynamic Loans*.

When adding a new fee, if you enable taxes on fees, then you can either choose to use the default tax rate source or not to apply taxes at all.

When [creating a new loan product](/docs/setting-up-new-loan-products#taxes), if in the **Taxes** section of the form you select **Value Added Tax**, and in the **Fees** section you select **Apply taxes to** > **Fees**, then all the fees are subject to taxation by default.

Besides the default behaviour, you have the option to mark a fee as being tax exempt by going to the **Fees** section and selecting **Nontaxable** under **Tax Source**, meaning that for the selected fee, the tax is neither going to be calculated, nor applied.

:::note

* Once the product is created, the tax source can no longer be edited.

* You cannot reduce the fee balance of products with Nontaxable Fees.

:::

## Manual fees

Manual fees can be applied to a loan account at any point in time. This type of fee applies when the event that triggers a fee application cannot be planned or predicted. For example: bounced cheques, lost cards, additional administration fees due to specific documents that had to be prepared, and so on.

For Manual fees, the available calculation options are:

* **Flat amount**: Can be set to a fixed amount if the fee amount is the same for all loans in this product or left empty, in which case you can enter the applicable fee amount on a case-by-case basis.

* **% of Disbursement Amount**: Calculated as a percentage of the approved loan amount.

## Planned fees

Planned fees are manual fees that can be set up in advance and added to the due date of future installments of all product types except for Revolving Credit. They represent an alternative to payment due fees, available for fixed loans only, but with added flexibility.

When planned fees are being set up, they appear in the loan schedule as part of regulatory or business requirements, and are only applied on the due date of the installment. This allows for timely notification of payments to customers and transparent loan schedules from the moment you create the loan.

Planned fees allow you to apply any sort of payment due fee you wish. They can be calculated externally at any time, and can be created to any installment you choose. You can adjust amounts whenever necessary, as long as they haven't been applied yet.

You can add planned fees at any point during a loan account's lifecycle, before or after disbursement.

Planned fees are automatically applied on their due dates, or they can be manually applied under the following circumstances:

* When performing a backdated disbursement, in the installments with exceeded due date.

* When entering a late repayment.

* When adding a new fee or editing an existing fee, in installments with exceeded due date.

:::warning

You may only apply planned fees in future installments if the installments are not in the **Grace** or **Payment Holiday** state.

:::

Planned fees are also available via API v2. For more information, see our [Loan Accounts - Planned Fees](/api/api-v2/loans/get-all-planned-fees/) in our API Reference.

If you need to pay off a loan, make early repayments or overpayments and you want to have all the fees applied on the schedule before you do that, you can apply one or more planned fees using the POST call of the `/api/loans//plannedfees:apply` endpoint.

:::note

Planned fees are not applied automatically when making early repayments or paying off a loan but they are applied on the due date of the installment, unless that installment is paid.

:::

Once the fee is applied, it is handled like a manual fee, in the following sequence:

* a transaction is logged

* accounting is logged

* the fee balance can be reduced, in which case a write-off transaction will be logged

## Editing planned fees

All planned fees can be edited at any time as long as they haven't been applied yet.

To edit a planned fee:

1. Open the loan account.

2. On the right-hand side of the screen, select **More** > **Edit Planned Fees**.

3. In the **Edit Planned Fees** dialog, make changes to any of the defined planned fees, delete all the planned fees, or add a new fee.

4. Select **Save Changes**.

## Applying planned fees

Planned fees, as the name suggests, are usually applied in future installments. You can also apply a planned fee on the account earlier than the due date of the installment if, for example, the client makes a repayment or a complete pay-off of the loan.

To apply one or more fees:

1. Open the loan account.

2. On the right-hand side of the screen, select **More** > **Edit Planned Fees**.

3. In the **Edit Planned Fees** dialog, you will see a list with all the planned fees per installment.

4. Select which fees you wish to apply on the next installment or select **Apply on Date** to apply the fee on another date during the installment period.

5. Select **Save Changes**.

:::note

* The Apply on Date functionality does not support time stamps. The fees will be applied at 00:00:00.

* The Apply on Date functionality cannot be set in the past, it needs to be set after the current organization date.

:::

## Deducted Disbursement fees

As the name suggests, this type of fee will be deducted from the approved principal amount at disbursement, meaning the client receives less money as actual disbursement, but still has to repay the full loan amount by the end of the loan term. In other words, the fee will be effectively "paid" upfront.

For deducted disbursement fees the available calculation options are:

* **Flat amount**: Can be set to a fixed amount if the fee amount is the same for all loans created under this product or left empty, in which case you can enter the applicable fee amount on a case-by-case basis. For example, if the fee amount is calculated based on a very specific formula or logic that Mambu doesn't automatically replicate.

* **% of Disbursed Amount**: Calculated as a percentage of the approved loan amount.

Additionally, disbursement fees can be either **Required** or **Optional** — the required fees will be applied to all loan accounts disbursed under this product, while the optional fees can be selected to be applied or not at disbursement.

:::note

Any additional **% of Disbursed Amount** fees added on the account after disbursement will be calculated based on the sum of the loan amount and the deducted disbursement fee amount.

:::

### Example

Loan amount = USD1,000

Deducted Disbursement Fee = USD100

Disbursed amount = USD900

Manual fee as 10% of disbursed amount = `(USD900 + USD100) * 10%` = USD100

## Capitalized Disbursement fees

As the name suggests, this type of fee will be added to the approved principal amount at disbursement, meaning the client receives the approved amount as actual disbursement, but has to repay a higher amount, including the loan fees, by the end of the loan term. Thus, the fees are effectively "paid" upfront but financed by the lender.

Capitalized Disbursement Fees are identical to the Deducted Disbursement fees in all other respects: same fee amount calculation options, as well as the "required / optional" feature, are available.

:::note

Any additional **% of Disbursed Amount** fees added on the account after disbursement will be calculated based on the sum of the loan amount and the capitalized disbursement fee amount.

:::

### Example

Loan amount = USD1,000

Capitalized Fee = USD100

Manual fee as 10% of disbursed amount = `(USD1,000 + USD100) *10%` = USD110

## Upfront Disbursement

As the name suggests, the upfront disbursement will be applied on the account as a “Fee” transaction, immediately after the account is disbursed and will be paid with one of the future payments. It can be selected when defining the disbursement details for a loan or when performing the disbursement.

Fixed Term Loans and Payment Plans will have the upfront fees automatically allocated on the first due installment and then you can change these fees when editing the schedule. Dynamic Term and Tranched Loans will have the fee marked as due immediately.

Upfront disbursement fees can’t be adjusted by themselves, but they will be automatically adjusted when the disbursement is undone.

:::note

A Tranched Loan product with required disbursement fees converts these required fees to optional on the next disbursement because they are meant to be applied only once during the loan's life cycle.

:::

## Late Repayment fees

Late repayment fees will be applied any time the client misses an installment. That installment is set to **Late** in the schedule.

For late repayment fees, the available calculation options are:

* **Flat amount**: It can be set to a fixed amount if the fee amount is the same for all loans under this product; since this fee is applied to all payments in the schedule in advance, it can't be left empty and specified on a case-by-case basis.

* **% of Disbursement Amount**: Is calculated as a percentage of the approved loan amount.

* **% of Repayment Principal Amount**: Is calculated as a percentage of the principal amount that was expected with the installment that was missed.

:::note

When triggered, the late payment fee will take into account the arrears tolerance period defined for that product. For example, if there is a tolerance period of two days, the late payment fee will only be applied to the account two days after the due date of the installment.

:::

## Payment due fees

The specificity of these fees is that they are calculated in advance and added to the loan's repayment schedule, along with the interest and principal due with each installment.

For payment due fees the available calculation options are:

* **Flat (€)**: It can be set to a fixed amount if the fee amount is the same for all loans under this product. Because this fee is applied to all payments in the schedule in advance, it can't be left empty and specified on a case-by-case basis.

* **Flat (€) / Num of Installments**: When the loan is disbursed, the fee will be charged on each installment based on the formula: `the flat amount of the payment due fee divided by the number of installments`.

* **% of Disbursement Amount**: Is calculated as a percentage of the approved loan amount.

* **% of Disbursement Amount / Num of Installments**: When the loan is disbursed, the fee will be charged for each installment, calculated as a percentage of the approved loan amount divided by number of installments.

In the **Fee Application** dropdown, choose to mark the fee as **Required** or as **Optional** at product level.

The Payment Due fees marked as **Optional** can be linked to the account when:

1. Creating the loan account, by clicking on the "+" icon and selecting the **Payment Due** fee from the dropdown menu from the **Disbursement Details** section.

2. Disbursing the loan account by selecting the Payment Due fee from the dropdown menu displayed on the **Disbursement** dialog.

The Payment Due fees (Required or Optional) will be displayed in **Disbursement Details** section at loan account creation and in the **Disbursement Dialog** at loan account disbursement.

:::note

Payment Due fees are not available for Tranched Loan products.

:::

### Fee included in Total Due

The **Fee included in Total Due** calculation method is designed for products where a fee - typically calculated as a percentage of the principal balance - must be integrated into the equal installment (PMT) formula:

`PMT = ( (Interest Rate + Fee Rate) / 12 , Number of Installments, -Loan Amount )`

This capability addresses regulatory or business requirements in various markets where financial institutions must include certain fees, such as insurance, as part of the total loan installment amount. These fees are characteristically calculated based on a percentage of the remaining principal.

To use this feature, you must create new Loan products with the following configuration:

* **Product Type**: Dynamic Term Loan

* **Interest Calculation**: Declining Balance (Equal installments)

* **Interest Type**: Simple Interest

* **Payment Method**: Optimized Payments

* **Prepayment Allocation**: On Upcoming Pending Installments Only (RNI)

* **Overdue Payment**: Increase Overdue Installments

**Fee Included in Total Due**

The Fee Included in Total Due fee type is found under the *Product Fees* section of the **Creating a New Loan Product** form. This fee is marked as Required and can be defined as a percentage (%).

Currently, no amortization profile is available for this fee type. The accounting rules for the associated General Ledger (GL) accounts follow the standard Mambu fee accounting structure.

This particular type of fee operates by mirroring both the interest accrual and penalty application mechanisms. It is accrued and applied on a daily basis.

In instances of late payments, the fee's value within the schedule is updated daily with its application, and it is specifically allocated to the corresponding late installment, adhering to the logic used for penalties.

When prepayments occur, the fee amount is recalculated based on the outstanding principal balance. Any accrued fee amounts are applied at the time of the repayment.

For this fee type, the following actions are permissible:

* Account closures (pay-off, write-off, reschedule/refinance)

* Fee rate changes

* Locking or unlocking accounts

:::important

If this fee type is configured at the product level, it will not be possible to configure Payment Holidays.

:::

:::info

If you wish to use the new **Fee included in Total Due** computation method, please get in touch with your Mambu Customer Success Manager or contact us through [Mambu Support](/docs/mambu-support) to discuss your requirements.

:::

## Arbitrary fees

Arbitrary fees can be applied manually to the accounts at any point during the accounts' lifecycle and with any given amount. By default, this option is not checked when creating a new product, so if you need to apply arbitrary fees to the accounts under that product, you must select the **Allow Arbitrary Fees** checkbox.

The difference between a manual and an arbitrary fee is that a manual fee is pre-defined, meaning it has a pre-set name and amount that the user can't change when applying the fee. An arbitrary fee is completely flexible—no predefined name and/or amount, it is up to you to input when applying such a fee onto the account.

Arbitrary fees should be used with caution. We recommend setting manual fees for more granular reporting and control.

## Fee amortization

Fee amortization is available for recognising up-front fees over the whole lifecycle of the loan. This option only becomes available if **Accrual Accounting** methodology is selected in the **Accounting Rules** section of the **Creating a New Loan Product** form.

:::warning Please be aware

For the Tranched Loan and Revolving Credit product types, there is no option to set up fee amortization profiles.

:::

After you add a fee as per the above steps, under **Product Fees**, you can choose an Amortization Profile.

There are three calculation methods (“Amortization Profiles”) available:

* [Sum-of-Year Digits](https://en.wikipedia.org/wiki/Depreciation#Sum-of-years-digits_method): A declining balance amortization that uses the number of installments and the sum of number of installments to calculate the amortization rate. This method is available only for *Deducted Fees*.